In 1997, Gary Wicnik founded Global Crossing, with a bold view of undersia fiber-optic cables to create a Global IP-based telecommunications network. It was a huge infrastructure game that was designed to form the main transport layer for the Internet, attach global data centers and network hubs.

However, the plan was not as far -sighted as it was, none of it is important in addition to an important element: The Last mileThe This final connection with the customer and the business has determined whether the network can fulfill its promise.

Global Crossing.com became one of the most hypod companies during the boom, which pic 47 billion dollar market capital. Demand for Internet bandwidth has increased – just as forecast. However, the bubble burst within 2001. The company enhanced its ability and could not earn enough income to cover its Debts. In January 2012, it filed a $ 12.4 billion responsibility for bankruptcy.

Lesson? You may be hurry and even right, but if you do not complete the journey, the opportunity goes away. As a growth investor, taking some profit is a reminder when the tension is higher. Not every rocket ship reaches the moon.

Ah, it was that day. I was trading technology and internet stocks on the 49th floor of the New York Plaza, such as a person in the hands of a person. Such a carrier-symmetrical action in the previous case! I even did business to GBLX but I made money or lost (probably lost) that I could not remember.

The last mile is why everything is finished

If my wife gets tired of listening to it has a mantra then it is: Finish the last mileThe Looking back, I did not fully appreciate the rise and fall of the global crossing like the way I manage today.

When you have no more fixed salary – since I didn’t quit my finance job in 2002 – there is no one to catch you when you slip. No meeting? Imagine! However, there is no pechk or no success. Everything depends on the ability to follow you.

In contrast, as an employee, you can take two weeks leave and still get paid. In larger companies, if you take three months subbatical, your absence can barely register. But when you are yourself – as a retireer, entrepreneur or solopranier – the last mile is on you.

Without finishing the final foot, not all plans, efforts and setups are nothing.

A recent missed last mile that still upset me

I’m sharing this story because I have dropped the ball and I want to be held accountable.

As part of the promotion Millionaire milestone: The simple steps of seven figures, I have given readers a unique opportunity for 1 -on -1 financial advice. Promotion: Buy 55 hard copies at a bulk quit, which will be roughly 40% lower than my general suggestion rate and get a private session in exchange. Clients can give books to books and I can help someone directly. Although I don’t make any money, it’s still a win.

This promotion ends on May 10 and my next book will not come back until the end of 2027 or in the middle of 2028. If you are interested you can complete the short form at the end of this page.

A client has accepted the offer. We have exchanged emails, and he has completed the onboarding questionnaire. I reviewed his information and he proposed a date and time. I am mentally confirmed that I opened my calendar, created a Google Meet invitation, wrote a note waiting for the call … and that was.

Unfortunately, I actually forgot Sending Calendar Invitation!

Close we went on the five-night Taho Ski trip. I even took a few suggestions during downtime and came back. But I didn’t understand the next Thursday morning that I never confirmed the meeting with him.

There was no email, no invitations were sent. Only silence at my end, I had a call with faith that it was my calendar.

When I finally responded and sent the calendar invites at the AT at the AT at AT, it was too late. His day was fulfilled. The worst, my last email to me was 11 days ago. 55 books and then imagine to listen to Nothing In return I felt terrible. My bad!

Why am I bad at meetings now (and what am I doing about it)

Meetings were everything in my finance days (1999-2012). When IPO Candidates Help the clients pitch, I can sometimes attend a 7-8 meeting in one day. It was timely and ready AL was not Chhik, it was expected. I often met clients for food or drinks. If I want to create a relationship I would have had no way to make them ghost.

But now? My average may be a business meeting in a week. I limit the advice in two sessions per month to protect my freedom and energy. That’s why you will not find my advice page even if you do not search. If it is easily discovered, my lifestyle will be reduced because demand is overwhelming.

The result? My “meeting muscle” has been atrophid. Sometimes I forget the appointments in my calendar. The alerts pop up, and I will still dismiss them mentally, as if they were disappearing. Since 2002, my brain has been re -worked on my schedule, not anyone else.

So here is what I started here:

Check my calendar every morning

Set two alarms for each meeting: 30 minutes ago and 5 minutes ago

Why are two alarms? Because I missed the meetings before a 30 minute closed. Oh boy … it takes time to rebuild for the meeting.

Success comes off the loop of success

You can constantly storm the brain, plan and prepare, but if you do not complete the final step, none of this is important. The last mile where the results occur. Here are some common examples:

1 Job victim

Plan: Create a biography, research agencies Miss: Never apply out of fear or avoid interviews Result: No job, no progress, no money

2 Fitness target

Plan: Buy Gear, Get a Instructor Miss: Don’t go consistently Result: No conversion

3 .. Start a business

Plan: Create a site, secured funds Miss: Never turn on Result: No Customer, No Revenue

4 Writing a book

Plan: 90%draft, correction Miss: Never reach agents, never reveal Result: Zero reader, zero effect

5. Investment

Plan: Do research, understand the risks and rewards Miss: Never invest Result: As your colleagues become more rich, the money left behind in inflation is lazy

6. Education

Plan: Pass the Exam, Join the class when you are not Hanggover Miss: Be just attended for three years and get down to start a band Results: Student Loan’s Degree and $ 60,000

7. Relationship

Plan: A fun opening line came up to reach Miss: Don’t call, never meet or send the message Result: Missed Connection, No Joy, No Love, No Child, Simply Loneliness

8. Financial plan

Plan: Create strategy, employ a financial professional, or take advantage of my promotion Miss: Don’t implement Result: Great plan, no results, and you will be full of regret at the age of 65

The finish line is where the magic occurs

We all know people who start with incredible power but never follow. I am guilty more times than I want to admit. But here is the truth: the real value, the increase, the award – it’s all the last mile life.

You are making a business, planning to retire or simply trying to keep your promise: finish the last mile. The world follows the award.

Readers, there are things that you have started but did not complete that important last mile? If that is what is left behind you?

Sometimes, a sign that has not ended is the time to move forward – and if the progress is postponed, departure can actually be intelligent choice. Do you have an instance where you have become a better decision to move away?

A perception after the truth: After sitting at 10 minutes with my wife at the dining table, he helped me realize a number of things. First, the client I forgot to send the invitation did not actually order 55 books – which is huge! It made me feel much less bad about forgetting to send me a calendar invitation. Second, the client could still follow several days later. Communication goes on both ways.

Order a copy of the Millionaire Milestones today

Great thanks to each of those who pre-order a hard copy Millionaire milestone: The simple steps of seven figures So far From what I am seeing, Amazon Currently provides the best price with the lowest price guarantee.

This book is my attempt to write a modern day version of the classic CrowdedThe Time has changed, and therefore there are several ways to achieve the Millionaire status.

Screenshot

Unfortunately, thanks for inflation, $ 3+ million faster new is becoming $ 1 million – and at the end of this decade, $ 5 million can take this title. Creating external resources without proper savings, investment and calculated risk is only becoming stronger.

Luckily for us, we have to overcome knowledge and resources. I wrote this book to help you soon gain financial independence, so that you can live in your terms. I hope you enjoy reading!

To celebrate the launch of my new book, Millionaire Milestones: Simple Steps To Seven Figures, on May 6, 2025, I thought it’d be fun to explore various millionaire topics leading up to the release.

For most millionaires, owning the nicest house they can afford is a top priority. Given that many of us are still spending more time at home post-pandemic, the intrinsic value of a home has gone up. And for millionaires with kids or a lot of furry friends, a spacious house on a large lot can feel like a necessity.

So in this post, let’s explore a fun question: How much income and net worth do you need to afford a $10 million home?

This topic is particularly interesting to me because I love real estate. When I purchased my current home in Q4 2023, I told myself I’d reached the top of my property ladder and didn’t want to climb higher. But there’s no harm in running the numbers just in case the economy roars back or I get lucky with an investment.

Minimum Income Necessary To Afford a $10 Million Home

When it comes to buying property responsibly, I like to follow the 30/30/3 home buying rule:

Rule #1: Spend no more than 30% of your gross income on your monthly mortgage payment.

If you’re financing the home, make sure the monthly mortgage doesn’t exceed 30% of your gross income. If you’re paying all cash, you should easily fall below this threshold.

Rule #2: Have at least 30% of the home’s value in cash (20% for the down payment, 10% as a buffer).

For a $10 million house, that means:

$2 million for a 20% down payment

$1 million as a cash reserve or liquid investments

This buffer is your safety net in case of job loss, an unexpected expense, or a major home repair.

Rule #3: Spend no more than 3–5 times your gross annual income on the purchase price.

Ideally, you’d earn at least $3.33 million a year to buy a $10 million home responsibly. That’s the 3X rule in action. You might stretch it and buy the home on a $2 million income if you have strong income stability and growth potential,but that’s a calculated risk.

Stretching to 5X your income means you’ll likely feel financially tight for at least the first year. If you go this route, here’s how to survive the most dangerous period after buying a home.

Minimum Net Worth Required To Afford a $10 Million House

After owning multiple homes over the past 22 years, I’ve found the sweet spot for your primary residence as a share of your net worth is no more than 30%. Ideally, it’s closer to 20%.

If you’re shopping for a $10 million home, this likely isn’t your first rodeo. You probably already have significant wealth and other investments. In contrast, the average American has over 70% of their net worth tied up in their primary residence.

A $10 million buyer might be:

A successful entrepreneur

A senior executive at a financial institution

A partner at a top law firm

A celebrity or professional athlete

A well-connected or corrupt government official who can trade with insider information

If your house represents more than 30% of your net worth, you’re at greater risk of financial stress during downturns, just like what happened during the 2008 Global Financial Crisis.

If your primary residence represents less than 10% of your net worth, you may be under-living relative to your financial capacity. That could be a sign to spend a little more on yourself or consider giving more away.

Ideal Net Worth Range

To feel financially secure with a $10 million home purchase:

Minimum net worth: ~$33 million (30% allocation)

Ideal net worth: ~$50 million (20% allocation)

With a $50 million net worth, you could comfortably pay cash or take on a smaller mortgage. Even if you take on an $8 million mortgage at 6%, your monthly payment would be about $48,000—easily manageable at this level.

Combining Ideal Income and Net Worth

Here’s a quick reference guide to safely buying a $10 million home:

Category

Amount

Minimum Income

$2 million/year

Recommended Income

$3.33 million/year

Minimum Net Worth

$16.7 million (at 60%)

Recommended Net Worth

$33.4 million (at 30%)

Ideal Net Worth

$50 million (at 20%)

If you only meet the minimum income requirement, make sure you have at least the recommended net worth. Conversely, if your net worth is on the low end, you’ll want your income to be on the higher side. Here’s a more comprehensive chart that highlights more homes at different price points.

Put Down More Than 20% If You Want To Buy A $10 Million House

If you’re planning to buy a $10 million home, it’s wise to put down more than just 20%. Most people I know buying homes in this price range are putting down 50%+, often paying all cash.

Why? Because many high earners making over $1 million a year don’t have high base salaries. Instead, their base is typically in the $250,000–$500,000 range, with the rest coming from stock grants and year-end bonuses. Banks may not fully recognize these forms of income when underwriting large mortgages given they are highly discretionary.

In today’s still-high interest rate environment, all-cash offers are also more attractive to sellers and more practical for buyers. Here’s what a mortgage would look like at 6%:

$8 million loan = ~$47,000/month

$7 million loan = ~$42,000/month

$6 million loan = ~$36,000/month

$5 million loan = ~$30,000/month

While these payments may be affordable if you’re making at least $2 million a year ($166,667/month), sticking to the rule of spending no more than 30% of your gross income on housing suggests a monthly cap of $50,000. That’s cutting it close with an $8 million loan.

The Ongoing Cost To Own A $10 Million Home

Owning a $10 million house doesn’t just mean a big upfront purchase, it means consistently large ongoing costs as well. Property taxes alone can range from $40,000 to over $300,000 a year, depending on your state. Hawaii offers the lowest property tax rates, while states like Illinois, New Jersey, and Texas are among the highest.

Beyond taxes, the cost to maintain a $10 million home adds up fast:

Higher heating and utility bills

More expensive homeowner’s insurance

Increased maintenance and repair costs

Costly landscaping and cleaning services

A larger mortgage payment (unless paid in cash)

And let’s not forget furnishing the place. It could cost well over $200,000. The bigger the house, the more expensive it is to make it feel like home. When something goes wrong—like a roof leak during a “Bomb Cyclone” as I experienced—it becomes much harder (and more expensive) to fix.

When evaluating a $10 million home, don’t just focus on the sticker price. Consider the cost of maintaining a $10 million house every year. Then factor in the opportunity cost of tying up so much capital in a primary residence that’s not generating income.

These ongoing costs are why you must follow my income and net worth guidelines by home price. If you don’t, your home could take you under.

Related: What’s It Like Living In An $18 Million Mega-Mansion?

$2.5 Million Income Family Budget Owning A $10 Million Home

Here’s a realistic breakdown of a family of four living in a high-cost area, earning $2.5 million a year:

Home: They put $3 million down on a $10 million dream home, taking out a $7 million mortgage at 6%, which costs them $504,000/year. Add ~$149,000/year for maintenance, taxes, insurance, and landscaping, and the total housing cost is around $653,000/year.

Kids: Their two children attend private grade school for $130,000/year, plus $5,000 in donations.

529 Contributions: They contribute $19,000/year for each child.

401(k) Savings: Each parent maxes out their 401(k) at $23,500/year (2025 limit), working toward millionaire status.

Despite the high expenses, they manage to save $373,140/year in their taxable brokerage accounts and have a $1M+ buffer in cash and liquid stocks for emergencies.

But here’s the risk: If one parent loses their job and household income drops by 50%, the family could be in serious trouble. Bear markets don’t just bring down investment portfolios—they also increase the risk of job loss.

Even a $5 million net worth, the absolute minimum I recommend to own a $10 million home, may not be enough. It all depends on how that net worth is structured. For instance, if $3 million is tied up in home equity and $1.8 million is in illiquid company stock that vests over three years, then having just $200,000 in cash won’t go far given their high burn rate.

Realistically, to own a $10 million home with minimal financial stress, a net worth closer to $33 million is more appropriate. At that level, you can weather market volatility, job loss, and unforeseen expenses. If you can’t sleep peacefully at night in your mansion, then what’s the point?

Should You Buy a $10 Million Home?

The best time to own the nicest house you can afford is when your kids are still living at home. So, I get why some of you might be browsing $10 million+ listings online. It’s fun to dream, and maybe you’re even serious about upgrading.

But even if you earn $2 million or more a year, I’m not convinced it’s worth buying such an expensive property. The upkeep alone can be a major downside, especially if the home wasn’t well built. I know a couple of people who bought $10+ million homes and ended up spending years trying to fix persistent leaks. What a nightmare.

Consistently making over $2 million a year is also no easy feat. You can ride a hot streak for a while, but the economy moves in boom-bust cycles. I saw this firsthand during my banking days, and I see it now as a small business owner. One year you’re up, the next you’re trying to stay afloat.

That’s why I believe you need a net worth of at least $33.3 million before buying a $10 million home. Your net worth is more reliable than your income, but even then, it’s not bulletproof. Just look at 2025, when tech stocks dropped more than 20%. If $30 million of your $33.3 million net worth was tied up in the Magnificent 7 companies, you’d be staring at a $6 million loss. Ouch.

Another factor: what are you upgrading from? If you’re jumping from a one-bedroom apartment to a 6,000-square-foot, six-bedroom mansion because your AI company IPO’d, that’s probably overkill. But if you’re trading up from a $5 million, 3,900-square-foot home with four bedrooms, the jump may be more reasonable. Further, you’ll have the experience to actually make use of the extra space.

For the sake of adaptability and long-term appreciation, a good rule of thumb is not to upgrade your primary residence by more than 100% in price. Beyond that, the risks and complexities start to outweigh the rewards.

A Better Way To Live In A $10 Million Home

While you’re working on building your income and saving up a down payment for that dream $10 million house, consider a smarter approach: invest in real estate to keep up with the market, without overextending yourself.

You might want to follow my BURL strategy, which stands for Buy Utility, Rent Luxury. The idea is simple: invest in properties that generate high rental income, and rent the luxury lifestyle instead of buying it.

If you follow this strategy, you could generate enough passive income to rent a $10 million home—and still have money left over.

For example, instead of buying a $10 million house at a 3% cap rate, which would generate just $300,000 a year in rental income, you could rent that same house for $300,000 a year. Then, invest the $10 million in higher-yielding multifamily properties at a 7% cap rate, and earn $700,000 a year in passive income.

After covering your rent, you’d still have $400,000 before taxes to spend or reinvest. Plus, your investment properties could appreciate over time, especially if they’re located in fast-growing, more affordable 18-hour cities.

By using the BURL strategy, you’re optimizing your capital and your lifestyle.

Order My New Book: Millionaire Milestones

If you’re ready to build more wealth than 93% of the population, grab a copy of my new book, Millionaire Milestones: Simple Steps to Seven Figures. With over 30 years of experience working in, studying, and writing about finance, I’ve distilled everything I know into this practical guide to help you achieve financial success.

The reality is, life gets better when you have a lot of money. Financial security gives you the freedom to live on your terms and the peace of mind that your children and loved ones are taken care of. You might even consider buying your $10 million water-view mansion on a large plot of land after reading my book.

Before you get to a $10 million net worth, you first have to reach the $1 million milestone. Millionaire Milestones is your roadmap to building the wealth you need to live the life you’ve always dreamed of. Order your copy today on Amazon and take the first step toward the financial future you deserve!

Click the image to pick up a copy on Amazon today

Earn More Passive Real Estate Income

Check out Fundrise, one of the leading real estate crowdfunding platforms with over 380,000 investors and approximately $3 billion in assets under management. With the economy in turmoil and stock market volatility running high, there’s a growing flight to more stable assets like real estate to help weather the storm.

Since 2016, I’ve invested about $1 million across various private real estate funds and deals to diversify away from my costly San Francisco real estate holdings. My goal has been to generate more passive income and capitalize on long-term demographic shifts toward the Sunbelt, where Fundrise concentrates much of its portfolio.

Fundrise is a long-time sponsor of Financial Samurai, and I’ve personally invested over $300,000 on the platform to date.

The Minimum Income And Net Worth Needed To Buy A $10 Million Home is a Financial Samurai original post. All rights reserved. Join 60,000 others and sign up for my free weekly newsletter here.

When it comes to saving for retirement, knowing which account to fund first is like knowing which steps to take when climbing a mountain. You want to reach the summit with enough oxygen (money) and energy (tax efficiency) to enjoy the view. For those aiming to retire early, funding retirement accounts in the right order and amount takes a bit more strategy.

Over the years, I’ve contributed to just about every retirement account out there—401(k), Roth IRA, SEP IRA, Solo 401(k), HSA, and good old taxable brokerage accounts. After retiring in 2012, I’ve had over a decade to keep funding these various retirement accounts to different degrees. A lot of what you can and want to contribute will depend on your income pre and post retirement.

So if you’re trying to figure out the best order to fund your retirement accounts so you can retire eary, let me walk you through what I believe is the optimal approach—one that minimizes taxes, boosts long-term returns, and gives you flexibility to live your best life in retirement.

The Ideal Order And Amount To Fund Your Retirement Accounts

To start, the main difference between a traditional retiree and an early retiree is simply the age of retirement. Traditional retirees typically stop working after age 60, while early retirees aim to do so before 60. As a result, early retirees need to accumulate enough capital and passive income to bridge the gap until they can access tax-advantaged retirement funds without penalty.

With that in mind, let’s walk through the ideal order to fund your retirement accounts if you want to retire early.

Step 1: Contribute to Your 401(k) Up to the Employer Match

Let’s start with the golden rule: never leave free money on the table.

Back when I was working in finance, my employer offered a 100% match on 401(k) contributions up to $4,000 for new employees. At the time, I was grinding hard in my 20s, working 60+ hours a week, and the idea of “free money” felt like a myth. But when I ran the numbers, I was pumped.

If you earn $80,000 and contribute 10% of your salary ($8,000), and your employer chips in ($4,000), you’re getting $12,000 invested each year. Over 30 years at an 8% return, that’s nearly $1.55 million vs. $1.06 million without the match.

Now that it’s been 26 years since I first contributed to a type of 401(k), I can clearly see the powerful effects of compounding. Accumulating your first million is the hardest, not the easiest, as I wrote in a previous post. But once you get there, your 10th million and every million after that comes much easier during normal times.

Step 2: Max Out Your HSA (If You Have a High Deductible Plan)

The Health Savings Account (HSA) is the only account that offers a triple tax benefit: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. The maximum contribution for 2025 is $4,300.

I wish I had started maxing out my HSA in my 20s and 30s, while paying for medical expenses out of pocket and letting the account grow. Had I done that, I’d likely have over $100,000 in additional tax-efficient retirement savings today. But back then, I didn’t fully understand my health insurance options, I just went with the default. Don’t make the same mistake. Ask your employer about all available health insurance plans and whether you’re eligible for an HSA.

That said, HSAs are only available if you’re on a high deductible health plan (HDHP). Make sure you have enough cash flow to cover surprise expenses, or this strategy could backfire. But if you’re healthy and can handle the risk, an HSA is a retirement powerhouse.

Step 3: Fund a Roth IRA

Once you’ve got your HSA sorted, it’s time to look at IRAs.

I wasn’t a fan of Roth IRAs until after I left work and had minimal income. But in hindsight, I could have contributed to a Roth IRA in my early years, which would have helped diversify my retirement portfolio.

When you withdraw from your 401(k), the IRS treats the withdrawals as ordinary income, not capital gains—which are typically taxed at a lower rate. This was one of my financial blind spots. I used to assume all investments would be taxed as capital gains. But with 401(k) contributions made pre-tax, your entire 401(k) balance ends up being one giant pot of tax-deferred income.

If you’re just starting your career and fall within the 24% federal marginal income tax bracket or lower, contributing to a Roth IRA makes a lot of sense. You contribute with after-tax dollars, your investments grow tax-free, and you can withdraw the money tax-free in retirement. Plus, there are no Required Minimum Distributions (RMDs), which provides valuable flexibility down the road.

2025 federal income tax brackets

Here are the latest Roth IRA income limits for 2025:

Single filers: You can make a full Roth IRA contribution if your income is below $150,000.

Married couples filing jointly: You can make a full contribution if your joint income is below $236,000.

If your income exceeds the limit to contribute directly to a Roth IRA, you can consider a Backdoor Roth IRA. That said, I believe the breakeven point for Roth contributions is around a 24%-27% marginal tax rate. If you’re in a 30%+ tax bracket, contributing heavily to a Roth IRA may not be as worthwhile. Instead, consider converting or contributing during years of low or no income.

The key is to choose based on your current tax situation. If you’re in a high-tax state and high income bracket, a Traditional IRA might provide more immediate tax relief. If you’re early in your career or retired with lower income, the Roth could be your best friend.

Ultimately, you want to maximize tax-free income in retirement. One of the best ways to do so is with a Roth IRA.

Step 4: Max Out the Rest of Your 401(k)

After you’ve handled the match, the HSA, and your IRA, go back and fill up the rest of your 401(k). The employee maximum contribution limit for 2025 is $23,500. The limit will likely increase every two years by $500 – $1,000.

Although potentially painful in the beginning, you will get accustomed to living on less and always maxing your 401(k) out. I treated my 401(k) contributions as a necessary expense, which made contributing much easier. That “sacrifice” has compounded into hundreds of thousands of extra dollars in retirement accounts.

Here’s my 401(k) savings guide by age if you want to see whether you’re on track. Based on my guide, I believe everyone who contributes at least $5,000 annually to their 401(k) and receives and employer match will become 401(k) millionaires by 60.

Step 5: Mega Backdoor Roth (If Your Employer Allows It)

This one’s not for everyone, but if your employer allows after-tax contributions to your 401(k) and in-plan Roth conversions, you’ve got yourself another way to diversify your retirement funds.

With the Mega Backdoor Roth IRA, you can potentially contribute up to $70,000 (in 2025) into your 401(k) and then convert it to a Roth. This is a huge opportunity for high earners to build more tax-free retirement wealth.

Here’s the logic behind doing a Mega Backdoor Roth IRA that I didn’t fully grasp when I was younger, mainly due to my dislike of paying taxes. If you’re going to invest using after-tax money in a taxable brokerage account anyway, you might as well funnel as much of that after-tax money as possible into a Roth IRA, where you can enjoy the tax benefits.

Again, Roth IRA investments grow tax-free and can also be withdrawn tax-free. It’s a no-brainer and something I regret not taking advantage of earlier in my life.

Just keep in mind that not all employers offer this option, so check with your HR department or plan administrator to see if it’s available.

Step 6: Invest Aggressively in a Taxable Brokerage Account

If you want to retire early, funding your taxable brokerage account is key. It is far more important than any other retirement account.

While there are no tax advantages, a taxable brokerage account is the most flexible investment vehicle. There are no income limits, no contribution caps, and no early withdrawal penalties. As an early retiree, it’s the dividend income and principal from your taxable brokerage account that you can tap to fund your lifestyle.

Your 401(k) and IRAs are great, but they’re locked up until age 59.5—unless you go through a Roth conversion ladder or use 72

As a target, aim to build your taxable portfolio to be 3X larger than your pre-tax retirement accounts by the time you want to retire. In other words, max out your 401(k) contributions first, then invest the same amount in your taxable brokerage account. As you earn more and get closer to retirement, strive to invest 2X (or more) of your 401(k) employee maximum into your taxable brokerage account.

This strategy helped me generate enough passive income to live off my investments in 2012 and focus on what I love.

Step 7: Earn Supplemental Income During And After Work

The final step for aspiring early retirees is to generate side income during work and after work. However, make sure you don’t violate your employee terms of agreement with your employer with your side hustle. Definitely don’t work on your side hustle during normal work hours. If you do, you will be warned, and might lose your job.

If you are a freelancer, you can open a Keogh 401(k) plan (also known as a Solo 401(k) or self-employed 401(k)) and contribute freelance income to it even if you already participate in a regular 401(k) through your employer. But you can only contribute a combined total of the maximum employee contribution for the year, e.g. $13,500 from as an employee, and $10,000 as a freelancer.

However, as a freelancer, you can also contribute as the employer to your Solo 401(k). Specifically, you’re allowed to make an employer contribution of up to 25% of your net self-employment income, in addition to your employee contribution.

The higher your net profit, the larger your employer contribution—up to a maximum of $46,500 for 2025. Combined with the employee contribution limit of $23,500, the total Solo 401(k) contribution limit for 2025 is $70,000.

Alternatively, you might find yourself in a dual-employment situation where one employer offers a 401(k) and the other provides a SEP-IRA. In this case, you could potentially contribute even more to pre-tax retirement accounts—assuming you and your employers earn enough to hit the limits.

Wonderful Retirement Benefits of Earning Side Income

The ability to contribute as both an employee and an employer can significantly boost your retirement savings. If your side business becomes increasingly profitable, you can also invest more into a taxable brokerage account. To max out the 2025 employer 401(k) contribution limit of $46,500, you’d need to earn a net profit of $186,000 ($46,500 ÷ 25%).

Best of all, a side hustle can provide a fun and meaningful purpose after early retirement. For me, being able to write on Financial Samurai and connect with readers over the years has been incredibly fulfilling. I can play sports all day.

In fact, during the two years leading up to retirement, I found myself more excited to wake up early and write posts and read comments than I was to go to my day job. So when the time came, the opportunity to focus on Financial Samurai with complete autonomy was simply too good to pass up.

Step 8: Negotiate Your Own Pension Through a Severance Package

Your final step to retiring early is negotiating your own pension package—in the form of a severance. If you’re planning to leave the workforce anyway, you might as well try. There’s no downside. Sadly, fewer than 15% of employers offer pensions today. That’s why you have to fight to build your own.

Too many employees either fear confrontation or mistakenly believe their employer would never offer them a severance for voluntarily leaving. These beliefs often stem from a lack of knowledge and emotional intelligence—specifically, the ability to see the situation from the employer’s perspective.

For example, if you’re a mediocre employee, your employer might want to let you go, but they’re stuck. Firing someone without proper documentation could expose them to legal risk. So instead, they have to initiate a performance improvement plan (PIP) that can take six months to a year.

On the flip side, if you’re a top performer, your employer will be reluctant to lose you. But if you offer to stay on during the transition and help train your replacement without disrupting productivity, they may reward your goodwill with a severance.

Our Two Severance Packages Were The Ultimate Catalysts To Retire Early

My own severance in 2012 covered five to six years of living expenses, essentially a mini pension that gave me the courage to live life on my own terms. Worst case, I could’ve gone back to work if things didn’t pan out.

My wife’s severance in 2015 gave her two years of financial runway. Even better, she returned to her old firm as a freelancer at a 60% pay bump with less stress and more flexibility. Less than a year later, we had our son, and she’s never gone back to work.

So please, for the love of all that’s good in this world—if you plan to retire early, try to negotiate a severance. You have more leverage than you think. Pick up a copy of How To Engineer Your Layoff to learn how.

A Simple Retirement Savings Framework To Keep In Mind

Max out tax-advantaged accounts = security after 60

Build taxable accounts for greater than your tax-advantaged accounts = freedom before 60

Your goal should be to take full advantage of all the tax-efficient retirement accounts available to you. If you don’t, you’re leaving money on the table that rightfully belongs to you. Thanks to hedonic adaptation—which works both ways—you’ll quickly get accustomed to maxing out your tax-advantaged retirement accounts.

Beyond that, your ultimate goal is to build your taxable investment portfolio to the point of maximum discomfort. If your monthly contributions to your taxable accounts still feel comfortable, you’re probably not contributing enough.

If you truly want to retire before 60, you must keep pushing your retirement contributions to the limit. Make it a game each month to see how much more you can save. If you’re still alive and kicking the next month, contribute even more.

Ultimately, if you can achieve a 50% savings rate after maxing out your tax-advantaged accounts, early retirement becomes a matter of when, not if.

Additional Tips For Optimizing Retirement Contributions

Watch fees. Stick with low-cost index funds from Vanguard, Schwab, or iShares. Avoid anything with an expense ratio over 0.25% unless you know exactly what you’re getting.

Keep it simple. As your wealth grows, so does the complexity. I’ve found it helpful to consolidate accounts under fewer institutions for better service and ease of tracking.

Stick to your strategy. Avoid emotional investing. Even though I invest in individual stocks, I keep ~70% of my public equities in index funds.

If you want to take your retirement planning to the next level, check out Boldin, a retirement-focused tool I’ve following and using since 2016.

It’s cheaper than hiring a financial advisor and gives you tools like Roth conversion calculators, real estate integration, and a holistic view of your portfolio. It has a free retirement planner for all to use. For an even more powerful option, its PlannerPlus version is just $120/year, and in my opinion, worth every penny if you’re serious about retiring well.

What I like about Boldin is that it doesn’t just focus on stocks and bonds—it also includes real estate, which makes up a significant portion of my net worth, as well as many Americans’. Conducting a comprehensive analysis of your entire net worth is essential for proper retirement planning.

Diversify Into Real Estate With Fundrise

If you want to diversify into real estate without the hassle of tenants and maintenance issues, check out Fundrise.

I’ve personally invested over $300,000 with Fundrise, a platform that gives you passive exposure to private real estate deals. They focus on Sunbelt markets where population and rent growth are strong, thanks to the rise of remote work.

What I like is that Fundrise combines the stability of bonds with the potential upside of equities, especially for those of us looking for diversification outside of the public markets. During times of chaos and distress, hard assets like real estate tend to outperform.

Subscribe To Financial Samurai

Finally, if you want more insights like this delivered straight to your inbox, make sure to subscribe to the Financial Samurai newsletter—over 60,000 people already have. My goal is to help you reach financial freedom sooner rather than later.

There’s no one-size-fits-all answer to retirement planning, but there is an optimal path depending on your income, goals, and lifestyle. There is on piece of advice relevant to everybody: Aggressively fund your retirement accounts while you still have the energy. Your future self will thank you.

Only when the stock market goes down people begin to wondering if they have too much exposure to their stock (equity). Questions raised: What should I cut back on? Can I buy a dive? What is the appropriate allotment to stock right now?

Although the answer depends on many variables – your risk tolerance, age, net price, current resources allocation and financial goals – the exact amount of stock exposure should not be complicated.

Examination of a common stock exposure litmus

Here is an easy way to determine if your stock exposure is appropriate if you are an working adult: here:

Count your paper damage when the latest market is modified and share that number by your current monthly income.

It gives you a rough estimate of how many months to work for the loss of your stock market by doing any return. This is part of my viewer’s formula that helps determine your true risk tolerance.

Examples of exposure to the stock market:

Let’s say you have a Million Million Portfolio, S&P 500 has been completely invested. If the market is fixed by 20%you lost $ 200,000. If you do $ 15,000 a month, you need to work 13.4 months To make up for damage.

If the idea of working extra month 13.4 does not surprise you – perhaps you are under 45 years of age, enjoy your job, or have lots of other resources – but your stock exposure may be right. You may even want to invest further.

But if the thoughts of working for a year only to recover your loss are frustrating, your exposure to your equity may be too high. Consider this to decrease and restart on more stable investments such as Treasury Bond or Real Estate.

A Real Case Study: Overxposed ways in stocks

Here I get a real example: a couple in the middle of the 50s in the middle of the year, consisting of $ 6.5 million worth of dollars, million million dollars in stocks and $ 500,000 in real estate. They do not spend more than $ 100,000 a year.

In the first four months of 2025 they lost 1 million from their stock portfolio, which declined to decline at $ 5 million. Maximum monthly expenditure is effectively lost with $ 8,333 (or ~ 11,000 gross) 90 months of total work income– it 7.5 years Simply work to restore their losses.

For couples in the mid-50s, it is unacceptable to lose so much time and money. They are already enough to survive ease. A 4% Return over Million Million Dollars in Treasury Bonds Risk Rs. 240,000 a year. It is twice the need for their expenditure with virtually any risk.

This couple is either chasing the return beyond the habit, their true risk is unknown about tolerance, or just never Worried financial directions receivedThe

I consult with more readers as part of me Million Promotion of the book, I understand that everyone has a financial blindspot that requires exclusion.

The best measure of time stock exposure

Why do we invest? Two main reasons:

Make money to buy things and experiences.

From Buy the time– So we don’t have to work forever in any of our choice jobs.

Time between the two is much more valuable. Your goal should not die with the maximum money, but you should still maximize your freedom and time when you are still healthy to enjoy it.

Of course, you can compare material things with your loss. For example, if you are enthusiastic of the car and your $ 2 million portfolio is reduced to $ 400,000, it’s four $ 100,000 dream cars. However, it is much more reasonable and powerful to measure the damage from time to time.

As you grow older it becomes more true – because you only have Short time Left.

There is a table that highlights multiple risk tolerance as measured in the work month. Your risk will be different. You can create the rest of the portfolio with bonds, real estate or other less unstable resources.

My personal views about time and stock exposure

Since I am 13, I think of most times than most of all. A friend of mine tragically died at the age of 15 in a car accident. The fact that I have reached life and money is deeply shaped.

I have studied hard, landed on a high pay in Finance, and reserve aggressively to reach financial independence at the age of 34. My goal was to retire by 40, but I have left after 34 Discuss a separation It covering the cost of living five to six years. I worked together with how I priced at time – it’s important than money.

Since retiring in 2002, I have kept my share at 25% -35% of my net price. Why? Because I refuse to lose more than 18 months during the average market recession, which happens every three to five years. This is my marginal. I never want to go back to work for someone else, especially I have a little baby now.

They say that you once won the game, stop the game. Yet here I am investing in risky assets, driven by inflation, Some greedAnd the desire to take care of my family.

Adjust stock exposure by time intending to work

In the previous example, I advised the couple to reduce their exposure or increase their expenses with Stock 6 million stock. Million in a downturn 1 million is equal to the total income of about 90 months based on their total income of $ 11,000/month.

If they feel more comfortable to lose the equivalent of only 30 months of income, their stock exposure should be limited to nearly $ 2 million. In this way, in a 16.7% modification, they will not lose more than $ 330,000.

Alternatively, they can justify their monthly income of $ 33,333 or about $ 400,000 a year to justify their million million dollars stock exposure. However, more easily, increase their next tax expenditure from $ 8,333 ($ 11,000 gross) to about $ 25,000 ($ 33,000). In this way, a million 1 million losses presents only 30 months of work or expenses.

Of course, increasing income is financially secure than increasing the cost. However, these lever you can lose your portfolio with your desire to lose time – you can pull the income, expense and assets allotment to pull.

If you have a $ 6.5 million net price and only $ 100,000 a year you are extremely conservative. 4% Rules suggest that you can safely spend $ 260,000 a year, which still gives you a lot of buffer. Therefore, this couple should survive more or pay more.

Spend maximum chance of time

I hope this structure helps you reconsider your stock exposure. It’s not about finding a perfect allocation. This is about to understand the cost of your opportunity and to align your investments with your goals.

Stock will always feel like Funny To me until they are sold and used for something meaningful. It is only when their values are finally realized.

If this recent downturn you are disappointed because you are lost, your exposure is probably too much. But if you are void and even more excited to buy more, your allocation is exactly exactly – or maybe too low.

Readers, how do you determine your appropriate amount of stock exposure? How many months of job income are you willing to lose for your possible loss?

Order my new book: Millionaire milestone

If you want to create more resources than 93% of the population and break free soon then hold a copy of my new book: Millionaire milestone: The simple steps of seven figuresThe I have experienced more than 30 years of experience in helping you become a billionaire — even many millioners. With enough assets, you can buy your time again, this is the most valuable asset.

Pick up a copy for sale Amazon Or wherever you enjoy buying books. Most people don’t take the time to read personal finance articles – write a book alone about creating financial freedom. By simply reading, you are already gaining a big advantage.

Financial Samurai started in the 21st and is one of the independently -owned private finance sites today. Since its inception, more than 100 million people have soon visited financial samurai to achieve financial independence.Sign up here for my free weekly newsletter.

আপনি ব্যবহৃত আউটডোর গিয়ার বিক্রি করার জন্য সেরা জায়গাগুলি জানতে চান? অতিরিক্ত অর্থোপার্জনের জন্য ব্যবহৃত আউটডোর গিয়ার বিক্রি করা অনেক কারণে জনপ্রিয়। লোকেরা তাদের গিয়ার আপগ্রেড করতে, তাদের ঘরগুলি ডিক্লুট করতে চায়, তারা যা কিনেছিল এবং আরও ভাল কিছু খুঁজে পায় না বা তাদের গিয়ারটি তার পরিবর্তে দ্বিতীয় বাড়ি দিতে চায় না …

আপনি কি জানতে চান? ব্যবহৃত বহিরঙ্গন গিয়ার বিক্রি করার জন্য সেরা জায়গা?

অতিরিক্ত অর্থোপার্জনের জন্য ব্যবহৃত আউটডোর গিয়ার বিক্রি করা অনেক কারণে জনপ্রিয়।

লোকেরা তাদের গিয়ারটি আপগ্রেড করতে, তাদের ঘরগুলি ডিক্লটার করতে চায়, তারা যা কিনেছিল এবং আরও ভাল কিছু খুঁজে পায় না বা তাদের গিয়ারকে কেবল ছুঁড়ে ফেলার পরিবর্তে দ্বিতীয় বাড়ি দিতে চায়। আউটডোর গিয়ার সর্বোপরি ব্যয়বহুল, তাই এটি বিক্রি করতে এবং আপনার কিছু অর্থ ফেরত পেতে সক্ষম হওয়া ভাল।

আপনি ভাবছেন, লোকেরা কি ব্যবহৃত বহিরঙ্গন গিয়ার কিনে? উত্তর হ্যাঁ! নিজেকে সহ আমি জানি অনেক লোক সারাক্ষণ ব্যবহৃত আউটডোর গিয়ার কিনে কারণ আমরা অর্থ সাশ্রয় করতে পারি এবং এখনও মানসম্পন্ন আইটেম পেতে পারি।

এই নিবন্ধে, আপনি শিখবেন:

ব্যবহৃত বহিরঙ্গন গিয়ার বিক্রি করার জন্য সেরা জায়গা

আপনি কী ধরণের বহিরঙ্গন গিয়ার বিক্রি করতে পারেন (এটি অনেক অনেক, যেমন হাইকিং গিয়ার, জুতা, ক্যাম্পিং আইটেম, স্কি সরঞ্জাম, পোশাক, বাইক, ফিটনেস আইটেম, ক্রীড়া সরঞ্জাম এবং আরও অনেক কিছু)

সফলভাবে ব্যবহৃত আউটডোর গিয়ার বিক্রির জন্য আমার টিপস

প্রস্তাবিত পড়া: আমার কাছে এবং অনলাইনে 27 সেরা কনসাইনমেন্ট স্টোর

ব্যবহৃত বহিরঙ্গন গিয়ার বিক্রি করার জন্য সেরা জায়গা

নীচে ব্যবহৃত আউটডোর গিয়ার বিক্রি করার জন্য সেরা জায়গাগুলির একটি তালিকা রয়েছে।

1। গিয়ারট্রেড

গিয়ারট্রেড ক্রেতাদের এবং বিক্রেতাদের সাশ্রয়ী মূল্যের আইটেমগুলির সন্ধানকারীদের জন্য একটি অনলাইন আউটডোর গিয়ার এক্সচেঞ্জ প্ল্যাটফর্ম। গিয়ারট্রেডে কেনা বেচা করার অনেক সুবিধা রয়েছে, যেমন:

আউটডোর গিয়ার দ্রুত তালিকা করতে সহজ তালিকা প্রক্রিয়া

অব্যবহৃত বা হালকা ব্যবহৃত গিয়ারকে নগদ হিসাবে পরিণত করে অর্থ উপার্জন করুন

হালকা ব্যবহৃত আউটডোর গিয়ার কিনতে খুঁজছেন বহিরঙ্গন উত্সাহীদের বিস্তৃত শ্রোতা

পোশাক, জুতা, ক্যাম্পিং এবং হাইকিং গিয়ার, স্কিইং এবং স্নোবোর্ডিং সরঞ্জাম, সাইক্লিং গিয়ার, ওয়াটারস্পোর্টস গিয়ার, ইলেকট্রনিক্স এবং আরও অনেক কিছু সহ আপনি গিয়ারট্রেডে সমস্ত ধরণের বহিরঙ্গন গিয়ার বিক্রি করতে পারেন।

আপনার যদি প্রয়োজন হয় তবে তারা আপনাকে একটি বিনামূল্যে শিপিং লেবেল এবং এমনকি একটি বাক্স প্রেরণ করে। আপনি তাদের যতটা চান তাদের পাঠাতে পারেন। যখন তারা আপনার বাক্সটি পায়, তখন তারা দেখতে পায় যে এটির মূল্য কী। যখন আইটেমগুলি বিক্রি হয়, তখন আপনি আপনার অর্থ পাবেন যা আপনি ভেনমো, পেপাল বা ক্রেডিট সঞ্চয় করতে পারেন।

আমি মনে করি এটি জেনে রাখা গুরুত্বপূর্ণ যে আপনার গিয়ারটি যদি 200 দিনের মধ্যে বিক্রি না হয় তবে গিয়ারট্রেড আপনাকে একটি ইমেল প্রেরণ করবে যাতে আপনি আইটেমগুলি দান করতে চান বা সেগুলি ফিরে পেতে চান কিনা তা জিজ্ঞাসা করে। আপনি যদি সেগুলি ফিরে চান তবে আপনাকে শিপিং ব্যয়ের জন্য অর্থ প্রদান করতে হবে। এবং, যদি আপনি 230 দিনের মধ্যে তাদের ইমেলের জবাব না দেয় তবে তারা সেগুলি দান করে (তবে, তারা আপনাকে এর আগে আপনাকে অনুস্মারক পাঠায়)।

2। আবার খেলাধুলা করুন

প্লে ইট অ্যাগেইন স্পোর্টস অনেকটা প্লেটোর পায়খানা (একটি ইট-ও-মর্টার শপ ব্যবহৃত আইটেমগুলি কেনা বেচা)। এটি আবার খেলুন স্পোর্টস নতুন এবং ব্যবহৃত স্পোর্টস এবং ফিটনেস সরঞ্জাম কেনা বেচাগুলিতে বিশেষীকরণ করে। এই জায়গাটি লোককে স্পটটিতে নগদ অর্থের জন্য তাদের নিজস্ব সরঞ্জামগুলিতে বাণিজ্য বা বিক্রয় করার অনুমতি দেওয়ার সময় লোকেরা গিয়ার কেনার অনুমতি দেয় (সুতরাং, একটি অনলাইন তালিকা তৈরি করার দরকার নেই, যা দুর্দান্ত!) বা ক্রেডিট সঞ্চয় করে।

আমি এটি আবার কয়েকবার খেলতে চলেছি, এবং এখানে সমস্ত কিছু এবং যে কোনও কিছুর একটি বিশাল নির্বাচন রয়েছে। আমি প্রায়শই ঘুরে দেখার পরামর্শ দিই যদি আপনি এমন কিছু সন্ধান করছেন তবে আইটেমগুলি ক্রমাগত স্টোরের বাইরে এবং বাইরে চলে যায়।

মার্কিন যুক্তরাষ্ট্রে বর্তমানে 290 টিরও বেশি স্টোর চলছে, তাই সম্ভবত আপনার কাছে কোনও স্টোর খোলা আছে। আপনি তাদের একটি কল দিতে পারেন এবং আপনি কী বিক্রি করতে চান তা তারা গ্রহণ করে কিনা তা দেখতে পারেন।

3। ইবে

ইবে একটি বিশাল শ্রোতা রয়েছে, এটি অনলাইনে ব্যবহৃত গিয়ার বিক্রি করার জন্য দুর্দান্ত জায়গা করে তোলে। অনলাইনে কয়েক মিলিয়ন সক্রিয় ব্যবহারকারী রয়েছে, এই ব্যবহারকারীদের মধ্যে বেশিরভাগই বিশেষত আরও সাশ্রয়ী মূল্যে আউটডোর গিয়ার খুঁজছেন।

ইবেতে একটি তালিকা তৈরি করা দ্রুত এবং সহজ, যা লোকেরা ইবেতে কেনা বেচা করা সহজ করে তোলে। ইবে এমনকি বিক্রেতার সুরক্ষা রয়েছে যাতে আপনার প্ল্যাটফর্মে বিক্রিতে আপনার আরও আত্মবিশ্বাস থাকে। আপনি নিলাম-শৈলীর তালিকা বা একটি স্থির-দামের তালিকার মধ্যেও চয়ন করতে পারেন।

আমার বোন ব্যক্তিগতভাবে ব্যবহৃত আউটডোর গিয়ার সহ ইবেতে প্রচুর পরিমাণে জিনিস বিক্রি করেছেন, সুতরাং এটি অবশ্যই বৈধ!

4। ফেসবুক

ফেসবুক আপনাকে স্থানীয়ভাবে বা শিপিংয়ের মাধ্যমে ব্যবহৃত আউটডোর গিয়ার বিক্রি করার বিকল্প দেয়। আপনার আউটডোর গিয়ারের জন্য একটি তালিকা তৈরি করার জন্য কোনও তালিকা ফি নেই এবং আপনি ফেসবুক মার্কেটপ্লেসে কেনাকাটা করা লক্ষ লক্ষ ফেসবুক ব্যবহারকারীদের অ্যাক্সেস পাবেন।

আপনি সরাসরি ফেসবুকের মাধ্যমে ক্রেতাদের সাথে চ্যাট করতে পারেন এবং স্থানীয়ভাবে আইটেমগুলি বিক্রি করতে পারেন, যা এখনই নগদ পাওয়ার এবং আপনার আইটেমগুলি থেকে দ্রুত মুক্তি পাওয়ার সুবিধা রয়েছে।

ফেসবুক মার্কেটপ্লেসে সফলভাবে বহিরঙ্গন গিয়ার বিক্রি করতে, আপনার আইটেমগুলির উচ্চ-মানের, ভাল-আলোকিত ফটোগুলি নিন এবং একটি বিশদ বিবরণ অন্তর্ভুক্ত করুন। কোনও অসম্পূর্ণতা বা ভাঙা টুকরা থাকলে অন্তর্ভুক্ত করুন। সর্বজনীন, ভাল-আলোকিত অঞ্চলে দেখা করুন এবং সর্বদা আপনার অন্ত্রের সাথে যান। যদি কিছু ঠিক মনে হয় না, এখনই ছেড়ে যান।

আপনি ফেসবুক গ্রুপগুলিতে যেমন হাইকিং এবং আউটডোর গ্রুপগুলিতে বা এমনকি আপনার অঞ্চলের স্থানীয় গোষ্ঠীতে আপনার ব্যবহৃত আউটডোর গিয়ার বিক্রি করার চেষ্টা করতে পারেন। আমি আমার ফেসবুক গ্রুপগুলিতে সারাক্ষণ বিক্রয়ের জন্য আউটডোর গিয়ার ব্যবহার করতে দেখছি।

5। পশমার্ক

পশমার্ক মূলত পোশাকের আইটেম বিক্রির জন্য পরিচিত, তবে আপনি এই প্ল্যাটফর্মে বহিরঙ্গন সরঞ্জামও বিক্রি করতে পারেন। পশমার্ক একটি অবিশ্বাস্যভাবে সহজেই ব্যবহারযোগ্য প্ল্যাটফর্ম, এটি আইটেমগুলি তালিকাভুক্ত করা এবং কেনা খুব সহজ করে তোলে। পশমার্ক একটি প্রিপেইড শিপিং লেবেল সরবরাহ করে, এটি আইটেমগুলি দ্রুত পাঠানো সুবিধাজনক করে তোলে।

পশমার্কে সফলভাবে আইটেম বিক্রি করার জন্য কয়েকটি টিপস এখানে রয়েছে:

সমস্ত কোণ থেকে আপনার আইটেমগুলির উচ্চমানের ফটোগুলি নিন এবং কোনও অসম্পূর্ণতা দেখান

শর্তটি সম্পর্কে সৎ হোন কারণ এটি ক্রেতাদের সাথে বিশ্বাস তৈরি করতে পারে

পশমার্ক মার্কেটপ্লেসে দৃশ্যমানতা বাড়াতে আপনার আইটেমগুলি নিয়মিত ভাগ করুন

6। পাতাগোনিয়ায় জীর্ণ পরিধান

পাতাগোনিয়ায় ওয়ার্ন ওয়েয়ার এমন একটি সাইট যা আপনাকে প্যাটাগোনিয়া আইটেমগুলিতে বাণিজ্য করতে দেয় যা আপনি আর চান না এবং তারপরে আপনার প্রয়োজন মতো নতুন জিনিসগুলিতে স্টোর ক্রেডিট পান।

এইভাবে পোশাক পরা কাজ করে:

“আপনার ব্যবহৃত পাতাগোনিয়া পোশাক এবং গিয়ার আমাদের প্রেরণ করুন এবং আমরা এটি পরবর্তী ব্যক্তির সাথে এটি পাস করতে সহায়তা করব যার প্রয়োজন হয় your আপনার আইটেমগুলি যদি যোগ্য হয় তবে আপনি প্যাটাগোনিয়া বা পরা পরিধানে অনলাইনে ক্রেডিট বা অনলাইনে ব্যবহার করতে এমএসআরপি (প্রস্তুতকারকের প্রস্তাবিত খুচরা মূল্য) এর 25% পর্যন্ত পেতে পারেন। আপনার গিয়ারটি এটি গ্রহণ করতে পারে না।

প্রথমে আপনার পাতাগোনিয়া পোশাক এবং আইটেমগুলি সংগ্রহ করুন যা এখনও কার্যকরী এবং ভাল অবস্থায় রয়েছে। তারপরে, $ 7 শিপিং লেবেল দিয়ে শিপিং করে বা কোনও পাতাগোনিয়া স্টোরের আইটেমগুলি ফেলে দিয়ে আপনার আইটেমগুলি পাতাগোনিয়াতে প্রেরণ করুন। শেষ অবধি, আইটেমটি ট্রেড-ইন করার জন্য প্যাটাগোনিয়ায় যোগ্য হলে আপনি স্টোর ক্রেডিট পাবেন।

এটি অবশ্যই প্যাটাগোনিয়া সম্পর্কে আমি পছন্দ করি!

7। রে/সরবরাহ

আরআইআই রে/সাপ্লাই ব্যবহৃত গিয়ার হ’ল জীর্ণ পরিধানের মতো একই প্রক্রিয়া, যা লোকদের স্টোর ক্রেডিটের জন্য তাদের ব্যবহৃত যোগ্য আরআইআই আইটেমগুলিতে বাণিজ্য করতে দেয়।

প্রথমত, আপনি আরআইআই -তে বাণিজ্য করতে চান এমন গিয়ারটি সংগ্রহ করুন। একটি আরআইআই স্টোরে আইটেমগুলি ফেলে দিন বা শিপিং লেবেল আরআইআই সহ 6 ডলারে সেগুলি শিপ করুন। অবশেষে, একবার আপনার ট্রেড-ইন সম্পূর্ণ হয়ে গেলে, আপনি আরআইআই গ্রহণকারী কোনও যোগ্য আইটেমের জন্য স্টোর ক্রেডিট পাবেন।

মনে রাখবেন যে আরআইআই এমন কিছু গ্রহণ করে না যা নির্দিষ্টভাবে আরআইআইতে বিক্রি হয় না, 6 বছরের বেশি বয়সী আইটেম, পরিবর্তন করা বা সংশোধন করা আইটেমগুলির পাশাপাশি কোনও ধরণের সুরক্ষা গিয়ারও।

8। আউট এবং পিছনে

আউট অ্যান্ড ব্যাক এমন একটি প্ল্যাটফর্ম যা নতুন এবং ব্যবহৃত বহিরঙ্গন আইটেম বিক্রি করে।

আউট এবং পিছনে আউটডোর গিয়ার বিক্রি শুরু করতে, আপনাকে একটি অ্যাকাউন্ট তৈরি করতে হবে এবং আপনার গিয়ারটি তালিকাভুক্ত করতে হবে। ফটো আপলোড করুন, একটি বিবরণ সরবরাহ করুন এবং আপনার বিক্রয় মূল্য সেট করুন।

আগ্রহী ক্রেতারা আপনার সাথে যোগাযোগ করবে এবং এটি যখন আপনি অর্থ প্রদান করতে পারেন এবং আইটেমটি শিপ করতে পারেন। আইটেমটি বিক্রি হয়ে গেলে, আপনি আউট এবং ব্যাক প্ল্যাটফর্মের মাধ্যমে অর্থ প্রদান পাবেন।

9। পুনরায় সাজানো

পুনরায় ব্যবহৃত একটি প্ল্যাটফর্ম যা ব্যবহৃত আউটডোর গিয়ার কেনা বেচা করতে বিশেষীকরণ করে। তাদের প্ল্যাটফর্মের টেকসইতা এবং বহিরঙ্গন ক্রিয়াকলাপগুলির পরিবেশগত প্রভাব হ্রাস করার উপর জোর রয়েছে।

এই প্ল্যাটফর্মটি বিশেষভাবে বহিরঙ্গন উত্সাহীদের দিকে প্রস্তুত, তাই আপনি ব্যবহৃত আউটডোর গিয়ারের জন্য আপনার সঠিক গ্রাহক বেসে পৌঁছাচ্ছেন এমন একটি ওয়েবসাইটে আপনার আইটেমগুলি বিক্রি করতে যাচ্ছেন।

10। স্থানীয় চালানের দোকান

স্থানীয় চালানের দোকানগুলি ব্যবহৃত আউটডোর গিয়ার বিক্রি করার জন্য দুর্দান্ত বিকল্প হতে পারে। তবে অনুশীলন বা বাইরে বিশেষজ্ঞের জন্য বিশেষায়িত কনসাইনমেন্ট শপগুলি সন্ধান করার জন্য আপনার যথাসাধ্য চেষ্টা করুন, কারণ এটি আপনার জিনিসপত্র চিরতরে তাকের উপর বসে থাকার পরিবর্তে বিক্রি হওয়ার সম্ভাবনা বাড়িয়ে তুলবে।

আপনি যদি এমন কোনও অঞ্চলে বাস করেন যেখানে প্রচুর হাইকিং ট্রেল, পার্ক বা এর মতো কিছু রয়েছে তবে সম্ভবত আপনার কাছে ব্যবহৃত আউটডোর স্টোর রয়েছে – আপনাকে কেবল কিছু অনুসন্ধান করতে হবে। এগুলি কম দামেও নিজের জন্য আরও গিয়ার কেনার জন্য দুর্দান্ত জায়গা।

মনে রাখবেন যে কনসাইনমেন্ট স্টোরগুলি আপনার বিক্রয়গুলির শতকরা শতাংশ নেয় যেহেতু তারা আপনাকে আইটেম (গুলি) বিক্রয় করতে সহায়তা করছে।

প্রায়শই জিজ্ঞাসিত প্রশ্ন

নীচে ব্যবহৃত আউটডোর গিয়ার বিক্রয় সম্পর্কে সাধারণ প্রশ্নের উত্তর দেওয়া হয়েছে।

আমি কোন ধরণের ব্যবহৃত আউটডোর গিয়ার বিক্রি করতে পারি?

আপনি তাঁবু, স্লিপিং ব্যাগ, ব্যাকপ্যাকস, হাইকিং বুট, রেইন জ্যাকেট, বাইক-প্যাকিং গিয়ার, কায়াকস, পোশাক (প্যান্ট এবং শার্টের মতো) এবং স্নোবোর্ড সহ বিভিন্ন ধরণের ব্যবহৃত আউটডোর গিয়ার বিক্রি করতে পারেন। আমি কেবল কয়েকটি আইটেম তালিকাভুক্ত করেছি, তবে মনে রাখবেন আপনি আউটডোর গিয়ারের সাথে সম্পর্কিত প্রায় কোনও কিছু বিক্রি করতে পারেন, তাই তালিকাটি অন্তহীন।

কীভাবে ক্যাম্পিং গিয়ার থেকে মুক্তি পাবেন?

আপনি অনলাইনে বা স্থানীয়ভাবে আইটেম বিক্রি করে বা একটি থ্রিফ্ট স্টোরে আইটেমগুলি দান করে ক্যাম্পিং গিয়ার থেকে মুক্তি পেতে পারেন। আশ্রয়কেন্দ্রগুলি সাধারণত তাঁবু, স্লিপিং ব্যাগ এবং উষ্ণ পোশাকের অনুদানও গ্রহণ করে। বয় স্কাউটস, গার্ল স্কাউটস এবং অন্যান্য বহিরঙ্গন শিক্ষা প্রোগ্রামগুলিও এই অনুদানগুলি গ্রহণ করতে পারে।

ব্যাককন্ট্রি কি ব্যবহৃত গিয়ার কিনে?

ব্যাককন্ট্রি ব্যবহৃত গিয়ার কিনে না এবং কেবল ব্র্যান্ড-নতুন আউটডোর আইটেম বিক্রয় করতে বিশেষী।

আরআইআই কি আউটডোর গিয়ার ব্যবহার করে?

হ্যাঁ, আরআইআই তাদের আরআইআই রে/সরবরাহ (পূর্বে ব্যবহৃত গিয়ার) প্রোগ্রামের মাধ্যমে আউটডোর গিয়ার ব্যবহার করে। যদিও ব্যতিক্রম আছে। আরআইআই আবার ক্লাইম্বিং গিয়ার, বাইক, হেলমেট, জোতা, জল পরিস্রাবণ সিস্টেম বা অন্তর্বাস কিনে না। আপনি এখানে আরআইআই বায়ব্যাক প্রোগ্রাম সম্পর্কে আরও জানতে পারেন।

গিয়ারট্রেড কত শতাংশ নেয়?

2025 হিসাবে, এবং যখন আমি বর্তমানে এটি লিখছি, গিয়ারট্রেড একটি টায়ার্ড কাঠামোর উপর ভিত্তি করে চূড়ান্ত বিক্রয় মূল্যের এক শতাংশ নেয়। নিম্ন-দামের আইটেমগুলির জন্য, তারা উচ্চতর কাট নেয়, $ 50 এর অধীনে আইটেমগুলির জন্য 70% –85%, 50% থেকে 144.99 এর মধ্যে আইটেমগুলির জন্য 50% –70% এবং 30% –50% থেকে 145 এবং $ 564.99 এর মধ্যে আইটেমগুলির জন্য 30% –50%। 565 ডলার বা তার বেশি দামের আইটেমগুলির জন্য, গিয়ারট্রেড 30% নেয়, যার অর্থ বিক্রেতারা বিক্রয়মূল্যের 70% পান।

কীভাবে ব্যবহৃত তাঁবু বিক্রি করবেন?

আপনার ব্যবহৃত তাঁবু বিক্রি করার জন্য কয়েকটি বিকল্প রয়েছে, সহ:

আউটডোর গিয়ার মার্কেটপ্লেসস (রে রে/সরবরাহ, পাতাগোনিয়ায় জীর্ণ পরিধান এবং গিয়ারট্রেড)

অনলাইন মার্কেটপ্লেস (ফেসবুক মার্কেটপ্লেস)

আউটডোর কনসাইনমেন্ট স্টোর

কোনও ব্যবহৃত তাঁবু বিক্রি করার আগে, তাঁবুটি সঠিকভাবে পরিষ্কার করুন, পুরোপুরি সেট আপ করুন, বিভিন্ন কোণ থেকে ছবি তুলুন, ক্ষতির জন্য পরীক্ষা করুন এবং তালিকার বর্ণনায় কোনও ক্ষতি ভাগ করুন।

আমার শ্যালক সম্প্রতি তিনি যে ব্যাকপ্যাকিং ভ্রমণের জন্য একটি ব্যবহৃত তাঁবু কিনেছিলেন, তাই লোকেরা অবশ্যই এগুলি কিনে!

আমার কাছে ব্যবহৃত আউটডোর গিয়ার বিক্রি করার সেরা জায়গাটি কোথায়?

আপনি কোথায় থাকেন তার উপর নির্ভর করে ব্যবহৃত আউটডোর গিয়ার বিক্রির সেরা স্থানগুলি পৃথক হবে। আমি “আমার কাছে আউটডোর গিয়ার বিক্রি করার সেরা জায়গা” এর মতো কীওয়ার্ড সহ একটি গুগল অনুসন্ধান করার পরামর্শ দিচ্ছি এবং আপনি কোথায় থাকেন তার উপর নির্ভর করে স্থানীয় আউটডোর গিয়ার শপগুলির একটি তালিকা উঠে আসবে। আপনি যদি আপনার ব্যবহৃত আউটডোর গিয়ার বিক্রি করার জন্য কোনও স্থানীয় জায়গা খুঁজে না পান তবে প্যাটাগোনিয়ায় আরআইআই রে/সরবরাহ, জীর্ণ পরিধান এবং গিয়ারট্রেড দেখুন।

ব্যবহৃত বহিরঙ্গন গিয়ার বিক্রি করার জন্য সেরা জায়গা – সংক্ষিপ্তসার

আমি আশা করি আপনি ব্যবহৃত আউটডোর গিয়ার বিক্রি করার জন্য সেরা জায়গাগুলিতে আমার নিবন্ধটি উপভোগ করেছেন।

ব্যবহৃত আউটডোর গিয়ার বিক্রির জন্য অনেক ভাল বিকল্প রয়েছে এবং আপনি যে পদ্ধতিটি বেছে নিয়েছেন তা নির্ভর করে আপনি আপনার জিনিসগুলি থেকে কত দ্রুত মুক্তি পেতে চান তার উপর নির্ভর করে।

আপনি যদি এই দুটি জায়গায় প্রায়শই কেনাকাটা করেন এবং স্টোর ক্রেডিট চান তবে রে/সরবরাহ এবং জীর্ণ পরিধান দুর্দান্ত বিকল্প। আপনি যদি স্টোর ক্রেডিটের পরিবর্তে অর্থের সন্ধান করছেন তবে গিয়ারট্রেড একটি দুর্দান্ত বিকল্প। আপনি যদি এখনই স্টাফ থেকে মুক্তি পেতে চান তবে স্থানীয় ব্যবহৃত আউটডোর স্টোর এবং ফেসবুক মার্কেটপ্লেস দুর্দান্ত বিকল্প।

Get excited! After over two years of writing and editing, I’m thrilled to finally share my upcoming new book with you: Millionaire Milestones: Simple Steps To Seven Figures! If you’ve enjoyed my writing on Financial Samurai over the past 16 years, you’re going to love this book out on May 6, 2025.

With over 30 years of experience working in finance, writing about finance, studying finance, and becoming a millionaire at age 28 in 2005, I’ve poured everything I know into this book. Millionaire Milestones is packed with practical, modern strategies to help you become a millionaire in your lifetime with the freedom to live life on your terms.

I believe almost anyone can become a millionaire, but the data tells a different story—only about 7% of Americans are millionaires, and that percentage drops if you exclude primary home equity.

Despite the abundance of financial advice out there, there hasn’t been a practical and powerful guide that simplifies the path to millionaire status. That’s where Millionaire Milestones comes in.

I want to make you rich and I want to make your children financially independent from you! And ultimately, I want you to build more wealth so you can be free.

What’s Inside My New Book

This book breaks down the data behind millionaire households and shows you how to build wealth through:

Stocks and Bonds

Real Estate

Alternative Investments

Entrepreneurship

Your Career

There isn’t just one way to become a millionaire. My goal is to help you master multiple strategies so you can not only reach seven figures but also build a foundation to become a multi-millionaire.

Not only will my book guide you in building far greater wealth than the average person, but it will also teach you how to spend it wisely to enjoy life responsibly and preserve it for generations to come.

With a looming recession and tremendous uncertainty in the economy and stock market, it’s now more important than ever to boost your financial acumen. The investment you make you financial knowledge could be the best investment of your life.

Click the image and pre-order a hard copy on Amazon today. I’ve also got a special promotion below.

Why Becoming a Millionaire Is Growing In Necessity

Thanks to inflation, becoming a millionaire today is almost becoming more of a requirement for financial security. Back in the 1980s, being a millionaire meant you were living a fabulous lifestyle. Today, having $1 million might mean a modest middle-class lifestyle, especially if you have kids and live in a big city.

With $1 million in investable assets, you can safely withdraw $30,000–$50,000 annually in retirement. Combined with Social Security, you’re doing well, but it’s far from living large.

As inflation continues to eat at our purchasing power, aiming for millionaire status grows in importance—and why Millionaire Milestones is here to help you achieve it. As a hard worker who doesn’t make excuses for life’s many challenges, I want you to live the life that you want and deserve.

Life As A Millionaire Is Better Than Not

Only the rich and the poor say money can’t buy happiness. But here’s the truth: money can buy freedom, options, peace of mind, and satisfaction.

The feeling of knowing you’ve worked hard and can now live life on your terms is unmatched. And if you’re a parent, there’s no greater joy than being able to provide for your family without constant financial stress.

Think about Millionaire Milestones as the modern-day version of the all-time classic book, The Millionaire Next Door. Times have changed, and in my new book, I share the latest strategies on how to build more wealth than most.

When you become a millionaire, life changes in meaningful ways:

Confidence grows. You gain the courage to pursue your passions and speak your mind.

Authenticity matters more than approval. You no longer have to pretend that you are someone you are not or toe the company line to keep a paycheck.

Boundaries become easier. You can tell those who’ve wronged you to take a hike—if you feel like it.

Family becomes a focus. You gain the courage to settle down and start a family.

Time works in your favor. You can retire earlier, maximizing happiness and freedom for longer.

Safety improves. You can live in safer neighborhoods and drive reliable cars that protect your loved ones.

Parenting becomes more rewarding. You can spend more time with your kids during their crucial early years and provide opportunities you didn’t have.

Worry less about rejection. Your kids’ futures don’t rest entirely on getting into top colleges or landing lucrative jobs they don’t like—they’ll have a safety net. Rejections will also sting less for you too, which means you’re more willing to take more risks and potentially gain greater financial reward and satisfaction.

Compete more effectively in a rigged system. The world may not be fair, but with more resources, you can help make it more just.

Generosity becomes easier. You gain the flexibility to start passion projects and help others for free. You can also contribute more to charity, which always feels better than receiving.

Comfort improves. And perhaps my favorite benefit of being a millionaire: you no longer have to endure the back row of Economy class next to the toilets! Such inconveniences build character, but eventually, it gets old and you want to enjoy the nicer things in life a little more.

Reaching a $3 million net worth that generated about $80,000 in passive income was my turning point. At age 34, in 2012, I walked away from a multiple six-figure job in investment banking. The money was great, but the freedom? That was priceless. Nothing beats the feeling of being able to do what you want when you want.

Here’s the amazing part: once you hit that first million in investable assets, the next million—and the one after that—gets easier and easier. Let’s make it happen!

Your One Life to Build Wealth

95% of people are missing out on the financial freedom they deserve. Millionaire Milestones is designed to teach you how to go beyond the average—beyond the people who don’t read personal finance books, listen to podcasts, or seek financial guidance.

You’ve only got one life to build wealth for yourself and your family. Why not learn how to make the most of it? With practical advice, proven strategies, and a clear path to financial independence, Millionaire Milestones is your guide to building lasting wealth and creating the life you’ve always wanted.

If you purchase five or more hard cover copies of Millionaire Milestones on Amazon or wherever you buy books, you will receive a FREE copy of my bestselling ebook How To Engineer Your Layoff, a $97 value. My book shows you how to negotiate a severance package and break free from a job you dislike.

Simply send a copy of your purchase receipt to the address below by May 10, 2025 and mention this limited-time promotion. Let’s make you a millionaire!

Click the image to order 5 hard copies for the special promo

For those of you who are Financial Samurai newsletter subscribers, I’ll be announcing additional exclusive promotions in the coming weeks as well. Stay tuned!

For those of you who wish to purchase bulk orders (25 or more copies), feel free to contact me at sales AT financialsamurai DOT com. I’m happy to speak and participate in virtual webinars for your conference or company. I’ve spoken at Meta (Facebook), Yelp, William & Mary, and many other great organizations. Financially secure employees are happier and more productive.

Advanced Praise For Millionaire Milestones

“As the pioneer of the modern-day FIRE movement, Dogen brings a fresh take on wealth-building strategies. Packed with practical advice on investing, entrepreneurship, and financial planning, this book empowers readers to surpass their financial goals and live the life they deserve.”

—Jamie Fiore Higgins, Author of Bully Market and ex- MD at Goldman Sachs

“Building durable wealth has never been simple or easy. The problem is compounded by the constantly changing financial landscape. What worked yesterday no longer works today. What works today may not be appropriate tomorrow. Fortunately, Sam Dogen’s Millionaire Milestones is an easy-to-read, clear-thinking guide to achieving that seven-figure nirvana. Sam never belabors the obvious nor trods the beaten path. His recommendations are always profoundly insightful, innovative, and fresh. And they are confirmed by his own personal success! If you haven’t been able to achieve the wealth you dream of, I recommend Sam’s book. It will kick-start you to a more financially rewarding life.”

—Bill Bengen, Father of the 4% Rule

Sam Dogen is one of the most original thinkers in personal finance. What sets Sam apart is extremely actionable insights, helpful benchmarks and doing it all while prioritizing his family!”

—Noah Kagan, CEO of AppSumo and NYT Best-selling author of Million Dollar Weekend

“Millionaire Milestones is the ultimate playbook for anyone ready to take control of their financial future. With clear, actionable strategies for investing, entrepreneurship, and wealth-building, Sam inspires you to think bigger and achieve more. This book isn’t just about money. It’s about creating freedom to live life on your terms.”

—Humphrey Yang, Personal Finance YouTuber with 1.5+ Million Subscribers

“With surgical precision and refreshing candor, Sam Dogen dismantles the mythology surrounding wealth creation and replaces it with something far more valuable: a realistic roadmap to financial independence. Drawing from his own journey from Wall Street grinder to self-made millionaire, Dogen doesn’t just tell you to save and invest — he shows you exactly how to think about money, deploy capital strategically, and avoid the psychological traps that derail even the smartest investors. The result is a masterwork of practical wisdom that transforms the complex into the actionable. For anyone serious about building lasting wealth while maintaining their soul, this book isn’t just useful — it’s essential.”

— Jimmy Soni, best-selling author of The Founders

“I grew up poor and in public housing, with no one to teach me about money or any good role models. Learning about money always intimidated me, but Millionaire Milestones is the first book I’ve read that makes everything make sense in an approachable way. Sam not only provides both the tactics and the strategies to help you make the most of your money but there’s a healthy dose of solid life advice to help you earn and save more. Highly recommended!”

—Ed Latimore, Author and Former Heavyweight Boxer

“Millionaire Milestones is an indispensable guide to building wealth at any stage of life. What I appreciated most about this book is that it doesn’t treat money as an end in and of itself, but rather as a means to a life well lived. Dogen breaks down how to live a rich life in way that’s accessible to everyone.”

—Simone Stolzoff, author of The Good Enough Job

Sam Dogen achieved millionaire status by age 28, and now he’s sharing the blueprint. In Millionaire Milestones, Dogen revitalizes Napoleon Hill’s timeless principles with seven clear, actionable steps. From uncovering your “why” to sharpening your focus and taking bold action, this book lays out everything you need to build the wealth and life you deserve.

—Joe Saul-Sehy, creator and co-host Stacking Benjamins

“Millionaire Milestones is going to change the way you think about money. Sam gives you a clear, step-by-step strategy to hit your seven-figure goals without having to sacrifice your life in the process. An essential addition to every enterprising person’s bookshelf.”

—David McKnight, author of The Power of Zero

Pre-order your exclusive copy of Millionaire Milestones: Simple Steps to Seven Figures today and take the first step toward financial freedom. And if you want to give the gift of financial freedom, don’t forget to take advantage of the special promotion above.

About the Author, Sam Dogen

Sam Dogen, 47, is the founder of Financial Samurai, a leading independent personal finance website with roughly one million organic page views a month. Everything is based off firsthand experience and expertise because money is too important to be left to chance.

A pioneer of the FIRE (Financial Independence, Retire Early) movement in 2009, Sam previously worked at Goldman Sachs and Credit Suisse before retiring at age 34 as a multi-millionaire. He is a graduate of The College of William & Mary and earned his MBA from UC Berkeley. Today, Sam’s passive investment income exceeds $300,000 annually. He lives in San Francisco with his wife and two children. In his free time, he enjoys playing softball, tennis, pickleball, and going all-in in poker.

Other books authored by Dogen include the bestsellers:

Buy This Not That: How To Spend Your Way To Wealth And Freedom (Portfolio Penguin 2022). An instant WSJ bestseller that helps you tackle some of life’s biggest challenges by encouraging you to think in probabilities.

How To Engineer Your Layoff: Make A Small Fortune By Saying Goodbye (Independent 2012, 6th Edition 2025). A one-of-a-kind book that teachers you how to negotiate a severance package and break free from a job you no longer enjoy. Both my wife and I negotiated six-figure severance packages in 2012 and 2015 and haven’t been back to work since.

If want to achieve financial independence sooner, join over 60,000 subscribers and sign up for my free weekly newsletter. Stay informed about the most important financial events and never miss a beat.

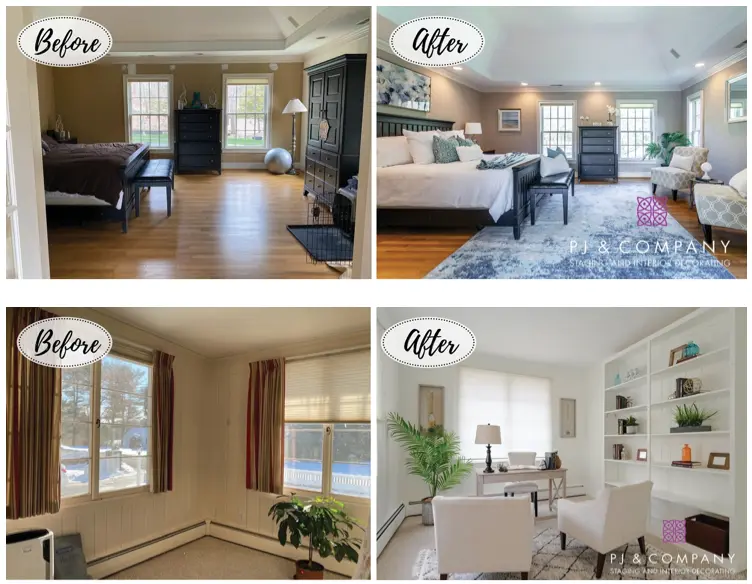

When it comes to selling a home, first impressions are everything. Yet, many sellers make the mistake of thinking buyers can look past an empty room, outdated furniture, or a poorly lit space. The reality? Most buyers have little imagination. They struggle to visualize a home’s true potential unless it’s presented to them in a polished, aspirational way.

This is why staging a home is one of the highest-ROI strategies you can use when selling. A well-staged home creates an emotional connection, helps justify a higher price, and speeds up the sale. In a competitive market, it’s often the difference between multiple offers and your listing sitting for months.

As someone who has bought and sold multiple properties, I’ve tested both approaches—selling staged and unstaged. The results? Staged homes always attracted more interest, leading to stronger offers.

I was skeptical about paying for staging for years. But in hindsight, the three best deals I ever purchased were on unstaged homes. There was far less competition, and the sellers were more receptive to my real estate love letters and quick-close offers. Sellers of unstaged homes often gave the impression they just wanted a quick sale with minimal effort and expense.

If you’re on the fence about staging, here’s why it’s worth it. I’ll also share the estimated cost to stage various types of property, as well as how to get staging done for free.

Most Buyers Can’t See Beyond What’s in Front of Them

It’s easy to assume buyers can picture how a home could look with their furniture and style. But most people struggle with spatial awareness. If they walk into an empty living room, they often can’t tell whether a sectional will fit. If a bedroom is poorly arranged, they might assume it’s too small for a queen-size bed, even if dimensions say otherwise. All these doubts put the brakes on submitting a strong offer.

This problem is even worse with outdated or unattractive interiors. A 2021 report from the National Association of Realtors (NAR) found that 82% of buyers’ agents said home staging made it easier for clients to visualize a property as their future home. Unstaged homes, especially those with strong personal decor or wear and tear, create doubt.

Buyers aren’t just shopping for a house; they’re shopping for a feeling. They want to step inside and instantly picture themselves living there. Take out those personalized items and pictures! If they have to work too hard to imagine that feeling, they’ll move on to a home that makes it easier for them.

Staging Helps Justify a Higher Price

The goal of staging isn’t just to make a home look nice, ultimately, it’s to increase perceived value. The better a home looks, the more buyers believe it’s worth.

A 2023 survey from the Real Estate Staging Association (RESA) found that staged homes sold for an average of 5-10% more than unstaged homes. This makes sense because buyers emotionally attach value to a space that feels move-in ready.

Let’s say you’re selling a home for $1 million. A 5% higher sale price from staging translates to $50,000 more in your pocket. Compare that to the $5,000–$8,000 you might spend on professional staging—it’s a strong return on investment.

The psychology behind this is simple. When buyers walk into a beautifully staged home, they assume:

The home has been well cared for

It’s in better condition than unstaged homes

They can move in with minimal effort

In contrast, an empty or poorly presented home invites doubts:

“Will my furniture fit here?”

“Does this awkward room layout work?”

“How much will I need to spend on remodeling?”

“Why is the seller so cheap? Is there anything else they are cheapening out on?”